How to do Core Banking Testing?

|

|

At the core of every bank, traditional or digital-only or neo-bank, is the Core Banking System (CBS). While mobile apps, web portals, and APIs are what you show to the customers, it’s the bank platform in the middle that actually moves money around, manages accounts, enforces rules, and ensures financial validity.

Core banking testing is very different from testing a UI-heavy SaaS product or even that of a digital banking app. Based on the ledger, it is rule-based (decisions), stateful, and does not have scope for errors. A single bug can lead to incorrect balances, violating regulations, and causing financial impact and systemic outages that reach tens of millions of customers.

Unlike front-ends that can allow some UI glitches, core banking systems must be mathematically, transactionally, and legally perfect every single time.

| Key Takeaways: |

|---|

|

What is a Core Banking System?

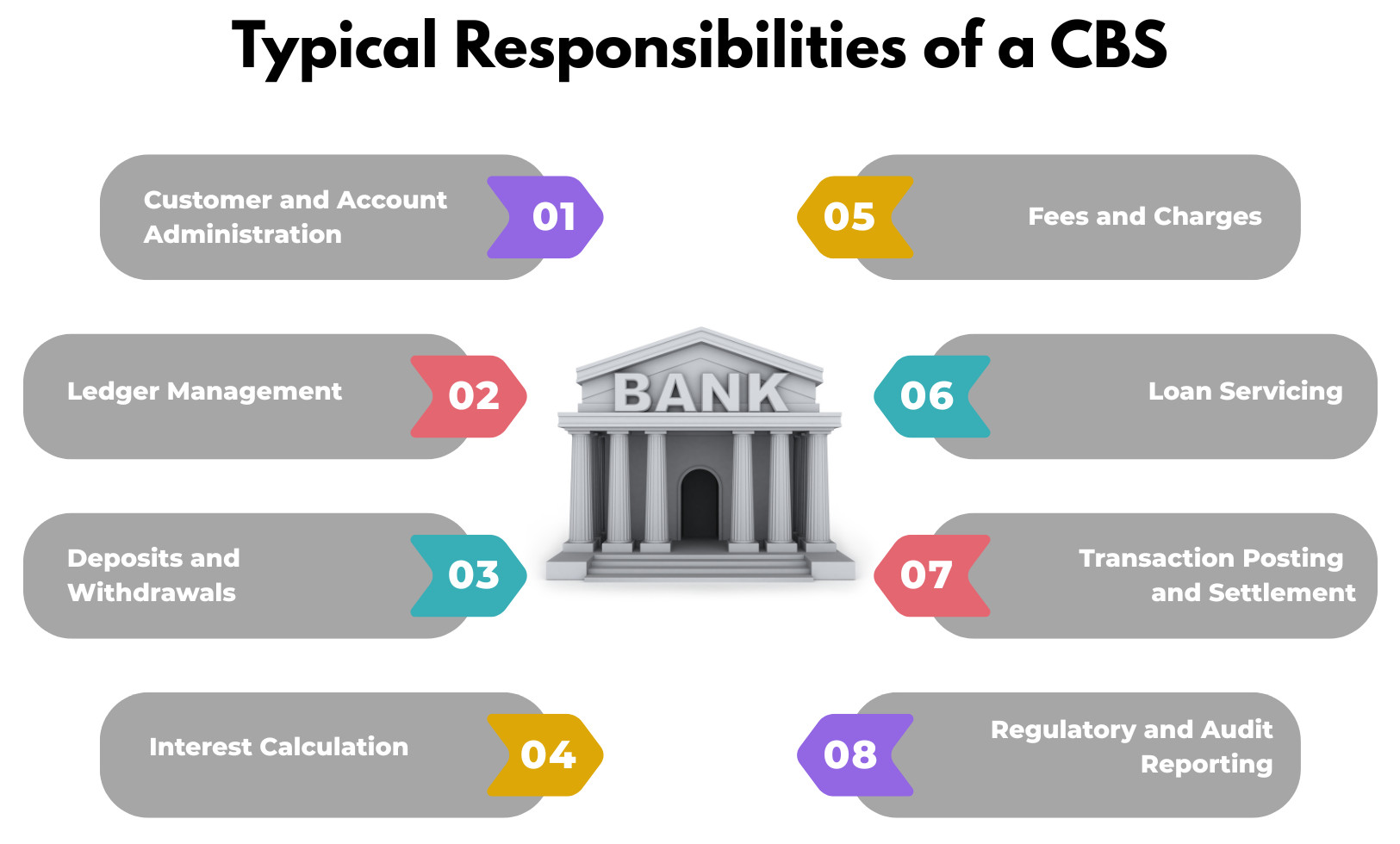

Typical Responsibilities of a CBS

- Customer and Account Administration: Provides full responsibilities for customer profiles as well as the management of all forms of accounts, such as opening, updating, or closing.

- Ledger Management (Double Entry): Maintains a record of all financial transactions in accordance with double-entry principles for proper and correct account balancing.

- Deposits and Withdrawals: Performs cash deposits and withdrawal transactions, as well as other transactions in real-time.

- Interest Calculation: Automatic interest calculation and application on deposits, loans, and credit products according to your rules.

- Fees and Charges: Applies service, penalty fees or charges as per the terms of the product and bank policies.

- Loan Servicing: Controls the entire life cycle of a loan, from disbursement, repayment schedule, interest accrual, to overdue processing.

- Transaction Posting and Settlement: Posts transactions to the relevant account and ensures that final settlement occurs across internal/external settlement systems.

- Regulatory and Audit Reporting: Generates accurate reports required for regulatory compliance, audits, and financial oversight.

All of the digital channels, including ATM, mobile app, branch software system, API, and payment gateway, interact with the CBS.

Read: How to Do AML (Anti Money Laundering) Testing.

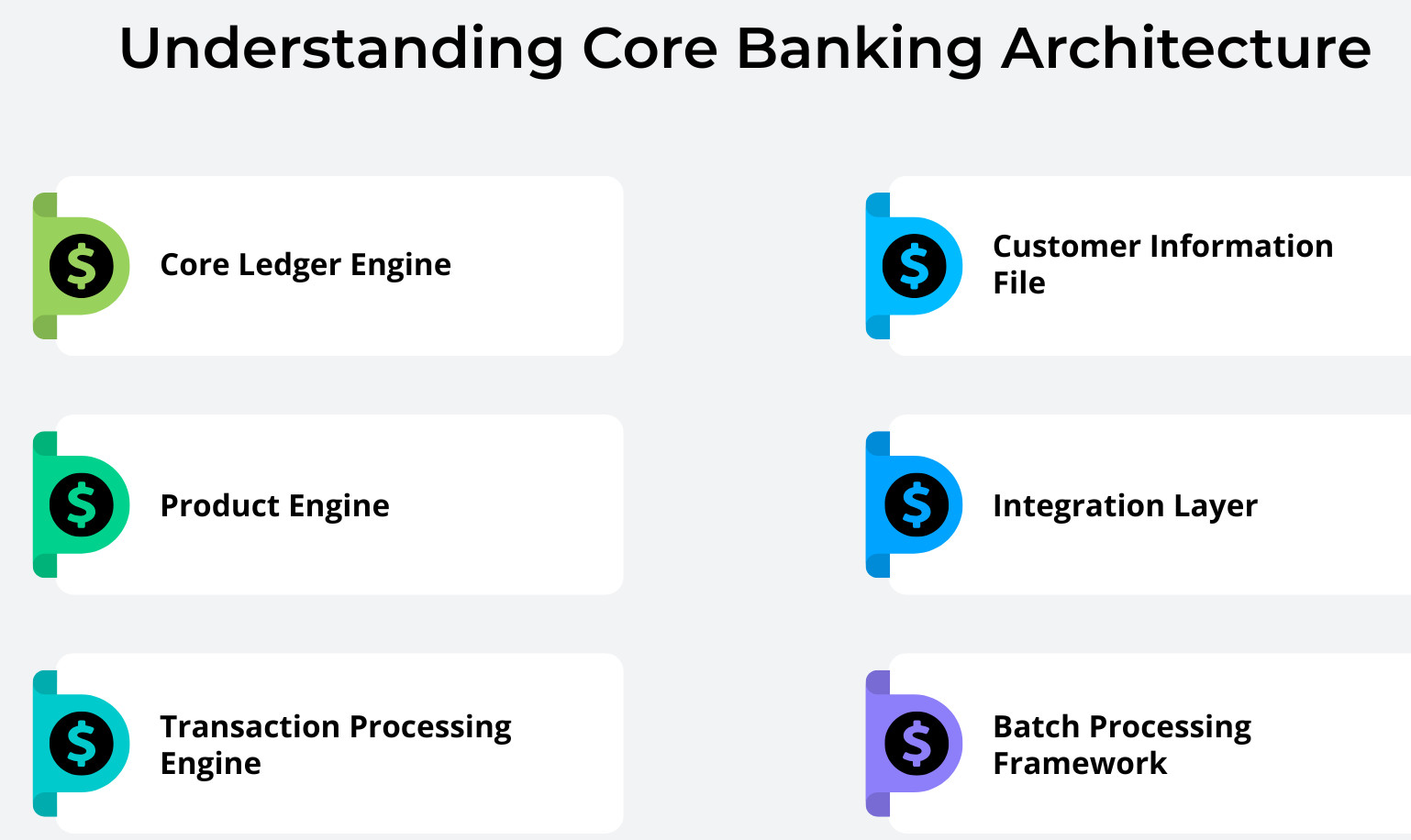

Understanding Core Banking Architecture

- Core Ledger Engine: The heart of the core banking application is the Core Ledger Engine, which ensures that all debit and credit transactions are recorded accurately and balanced, manages individual account balances, etc. It imposes strong constraints on the accounting and maintains atomicity and consistency, ensuring that all financial transactions are processed consistently and correctly without data corruption.

- Product Engine: Represents the decision processes for banking products, including savings, current, and term deposit account types. It is responsible for interest computations, fees and penalties, and enforces eligibility rules to ensure that the product is offered and works in accordance with bank policy.

- Transaction Processing Engine: Orchestrates the execution of all real-time and batch transactions throughout the bank. It enforces posting policies, enables reversals and edits, and verifies that transactions are batched appropriately by the established cut-off times.

- Customer Information File (CIF): Central repository of customer identity, KYC status, risk profile, and relationships across accounts.

- Integration Layer: The integration layer provides a scalable communication channel between the core banking solution and external or own stream systems. It enables secure and reliable data exchange across digital channels, payment networks, fraud/AML engines & customer engagement platforms over APIs, messaging queues, or via middleware.

- Batch Processing Framework: Processes high volumes of business transactions, performed on a scheduled time basis. It processes end-of-day and end-of-month tasks such as posting of interest, payment order generation, and financial reconciliation to maintain data integrity and system stability.

Read: Test Automation for FinTech Applications: Best Practices.

Why Core Banking Testing is Exceptionally Challenging

The testing of a core banking system extends well beyond functional verification, affecting the accuracy of financial data, customer confidence, and regulatory adherence. Even a small mistake can result in incorrect money flow, lawsuits, and unrecoverable data discrepancies, making precision absolutely critical.

Key Risk Factors

Core banking systems process real money, are heavily regulated and support very large numbers of transactions every day. Any breakdown can lead to financial losses, regulatory breaches and damage to the bank’s reputation.

Moreover, CBS systems depend on long-lived stateful processes with intricate dependencies spanning various internal and external systems. With no tolerance for data corruption, small errors can ultimately lead to system and audit failures at the end of the chain.

A flaw in a core banking system could misstate customer balances, break audit trails, and result in crippling regulatory fines. These types of failures completely subvert financial integrity, and at scale, customer trust will erode quickly. Consequently, core banking testing requires significantly more accurate, reliable, and validated results than traditional enterprise software.

Objectives of Core Banking Testing

- Functional Accuracy: All transactions had to be processed exactly as the business rules specified, the product was configured, and accounting guidelines demanded. Even small differences in transaction behavior may result in incorrect balances and reconciliation problems further downstream.

- Financial Integrity: Balances on the ledger must always tie out from all accounts, systems, and time periods. Testing will ensure that no transaction has imbalanced, duplicated data or missing financial data for any such situation.

- Performance and Scalability: The core banking system has to be able to cope with peak transaction volumes, end-of-day spikes, and batch-heavy processing windows. Performance testing ensures that the system is responsive and stable under heavy load.

- Security and Access Control: Unauthorised access to the core banking platform causes serious financial and legal damage. Testing needs to check for strong authentication, role-based access controls, and full audit logging to enforce and uncover misuse.

- Regulatory Compliance: Regulatory adherence is mandatory for all banking operations and cannot be compromised. Testing validates compliance with KYC/AML, PCI-DSS, SOX, GDPR, and country-specific banking regulations to avoid penalties and legal exposure.

Types of Core Banking Testing

Core banking requires more testing dimensions than almost any other system. It must support high-volume transactions, strict regulatory compliance, real-time processing, and uninterrupted availability across multiple channels. Even a minor defect can have widespread financial, legal, and reputational consequences, making exhaustive and multi-layered testing absolutely critical.

Functional Testing in Core Banking

- Account Lifecycle Testing: Holistic account journey testing validates the entire lifecycle of a customer account from creation to termination. It includes consistent state transitions such as open, sleeping periods, re-open, and closure, in addition to valid fields and an audit trail at each stage.

- Transaction Testing: The transaction testing verifies all financial transactions or movements within the core banking system. It provides for the correctness, atomicity, and consistency in deposit, withdrawal, funds transfer, standing instructions, as well as proper processing of failed/reversed transactions without accounting error.

- Interest Calculation Testing: Interest computation testing makes certain that the interest accrual and posting logic is mathematically accurate and adheres to banking policy. It further ensures that edge cases, such as leap years, mid-cycle rate adjustments, and different posting frequencies, are properly validated to avoid customer disputes and revenue loss.

- Fees and Charges Testing: Ensures that all penalties, service fees, and taxes are accounted for per the service offering rules and transaction type. It plays a role in transparency by confirming that deductions, reversals, and customer notifications are still being done correctly.

- Loan Processing Testing: Ensures the entire loan lifecycle, including EMI schedules, part payments, foreclosures, and delinquency, is validated. It guarantees interest-based re-computation, penalty implementation, and compliance with lending laws that are relevant to the changing repayment scenarios.

Functional tests must validate normal, boundary, and abnormal scenarios to ensure the system remains stable, accurate, and compliant under all operational conditions.

Read: Functional Testing Types: An In-Depth Look.

Ledger and Accounting Testing

- Double-Entry Accounting Validation: Validation of double-entry accounting means that each financial transaction complies with basic accounting principles. Every transaction has to hit (and it only hits) one account on the debit side and another account on the credit side, summing to 0 at a system level to keep accounting in order.

- Ledger Reconciliation Testing: Used to ensure synchronisation of data between various levels in the ledger of the core bank application. And, it does so by guaranteeing that account-level balances are in sync with general ledger balances and sub-ledgers are synchronized to the general ledger, and that both intra-day and end-of-day reconciliations balance without error.

- Posting Rules Testing: Verifies that transactions are posted as per proper order, value date, and accounting heads. This is necessary to maintain accurate financial reports, as well as correct calculations of interest and fees, and to be in accordance with accounting rules and the law.

- Reversal and Adjustment Testing: Ensures that incorrect or exceptional transactions can be corrected without breaking accounting consistency. It validates full reversals, partial reversals, and back-dated adjustments while maintaining a complete audit trail and accurate balances.

Even a single incorrect posting rule can corrupt financial statements and create widespread financial and compliance risks across the banking system.

Batch Processing and EOD Testing

- End-of-Day (EOD) Testing: Ensures that all daily banking processes receive a correct close-off after transaction cut-off times. It keeps interest calculation, rollover of balance, statement generation, and settlement entries posting correctly without any discrepancy.

- End-of-Month (EOM) and End-of-Year (EOY) Testing: EOM and EOY testing ensure that cyclical financial activities (i.e., posting of interest, calculation of taxes, and reporting for regulatory requirements) are calculated accurately. It also includes accountability, age verification, and ensures data integrity throughout long-term financial cycles.

Batch failures can halt banking operations, so testing must validate success paths, retry mechanisms, rollbacks, and recovery scenarios to ensure operational resilience.

Integration Testing for Core Banking

- Channel Integration Testing: Ensures a smooth flow of transactions between core banking and customer touch-point channels, including mobile banking, internet banking, and ATMs, as well as teller systems at branches. It provides consistent balances, live updates, and the same business rules for all access points.

- Payment Systems Integration: Integration testing with payment systems ensures the successful processing of local and international payment networks, including NEFT, RTGS, ACH, SEPA, and SWIFT. It checks the format of messages, settlement confirmation, and the correct completion of transactions with respect to declined, delayed or rejected payments. Read: How to Do Payments Testing: Ensuring Secure and Seamless Transaction Processing.

- Fraud and AML Integration: Integration Testing for Fraud and AML ensures that transactions are being checked against risk and compliance engines, in real-time or near-real time. This guarantees accurate risk scoring, block and report of true-fraud decisions without affecting true customer transactions.

- Third-Party Systems: Integrations with third-party providers, including credit bureaus, tax authorities and identity verification solutions, have also been tested independently. It makes sure data transfer is precise, decisions are made correctly, and fallback behavior is consistent to prevent service downtime or latency problems.

Integration testing must validate data consistency, timing, and failure handling to maintain system stability, compliance, and customer trust across the banking ecosystem.

API Testing for Banks

- API Functional Validation: Ensures the correctness of the request and response payload between systems. It provides some consistency on enforced mandatories, schema compliance, and business rule validations.

- Security Testing: Verifies that APIs are secure from unauthorized access and usage. It makes sure that tokens’ lifecycle is handled properly, scopes are honored, and rate limiting rules are applied.

- Idempotency Testing: Tests for the condition that multiple API requests do not produce duplicate financial transactions. This ensures that financial data will be accurate with retries, network disconnections, etc.

- Failure and Timeout Handling: Validates system behavior during partial failures or delayed responses. It ensures retry logic and compensation mechanisms work correctly without causing data corruption or financial inconsistencies.

APIs are often the weakest link in core banking systems if not tested rigorously, making comprehensive validation essential for system stability and security.

Read: How to do API testing using testRigor?

Performance and Load Testing

- Load Testing: Verifies the system’s performance under normal and peak conditions that might be encountered in daily usage (including salary credit days, seasonal festivals, and end-of-year processing). It provides predictable response times and sustained throughput during peak times of your applications.

- Stress Testing: Evaluates how the system works under transaction loads that exceed its anticipated capacity. It can also help you find breaking points, what happens when a resource runs out, and how the system recovers from extreme situations.

- Endurance Testing: Involves validating system stability during process execution (e.g., long-running batch jobs). It notices memory leaks and DB contention, slow-by-slow or over time.

Performance metrics include transactions per second (TPS), posting latency, and batch completion time, which collectively measure the system’s ability to handle scale and time-critical banking operations.

Read: What is Performance Testing: Types and Examples.

Security Testing in Core Banking

- Authentication and Authorization Testing: Ensures that users have access only to what their role allows. It verifies role-based access controls, segregation of duties, and eliminates privilege escalation for the entire system. Read: Authentication vs. Authorization: Key Differences.

- Vulnerability Testing: Identifies weaknesses that attackers or insiders could exploit. It focuses on threats such as SQL injection, misuse of privileged access, and insecure system or configuration settings.

- Audit Trail Validation: Verifies that all software activity is accurately captured and cannot be modified. It offers full business transparency from each transaction to its originator for compliance and forensic analysis.

Regulatory and Compliance Testing

- KYC and AML Compliance: Validates customer verification processes and ongoing transaction monitoring. It ensures correct threshold enforcement, accurate reporting, and timely flagging of suspicious activities.

- Data Privacy Compliance: Ensures that personally identifiable information is protected throughout its lifecycle. It validates PII masking, data retention rules, and proper consent management in line with privacy regulations.

- Audit Readiness: Ensures the system can withstand regulatory inspections at any time. It validates traceable transaction histories, immutable audit logs, and the ability to generate accurate, reproducible compliance reports on demand.

Read more: AI Compliance for Software.

Test Data Strategy for Core Banking

- Synthetic Data: This is artificially created based on real banking regulations and formats. It contains real account numbers, national identifiers, and realistic transactional patterns that resemble production data without revealing sensitive values.

- Masked Production Data: These real datasets, whose sensitive components have been fully obfuscated or tokenized, are used to simulate masked production hosts. Maintains referential integrity and data distribution, while making sure that the original customer identities cannot be reconstructed.

- Scenario-Based Data: Contextual data is intended to support a given banking context or edge case. Comprises inactive accounts, overdrawn accounts, and high-risk customer types to test the system under exceptional and regulation-driven conditions.

Read: Test Data Generation Automation.

Automation Challenges in Core Banking Testing

Traditional automation struggles in core banking because user interfaces change frequently, workflows are long and highly stateful, and data dependencies are deeply interconnected. A large portion of core banking validation happens in batch jobs and backend processes, where UI-centric and script-heavy tools offer limited coverage. As a result, these tools become brittle, costly to maintain, and slow to adapt to evolving banking systems.

testRigor addresses these challenges by enabling plain English test creation, resilient UI and API automation, and strong backend validation, significantly reducing maintenance effort while supporting complex, end-to-end core banking workflows.

- Natural Language Scripting: With testRigor, even manual testers can create automation scripts in plain English. Thanks to the Natural Language Processing algorithms, AI context, and Vision AI, these help not just manual testers, but everyone on the team. People without coding knowledge can create or update automation scripts very easily. This helps to increase the automation coverage by automating any edge cases.

- No Flaky Tests: They are mainly caused by the element locator error. It’s common that element properties get changed frequently, and the traditional tools, where whole automation relies on element properties, fail miserably, creating a high magnitude of flaky tests, thereby not giving any proper insight to the product management team. testRigor uses its own ways of identifying the element. Using testRigor, you can specify the element name or its position, and it will identify the element. So, the flakiness reduces to zero, and therefore, maintenance is also minimal.

Read: Decrease Test Maintenance Time by 99.5% with testRigor.

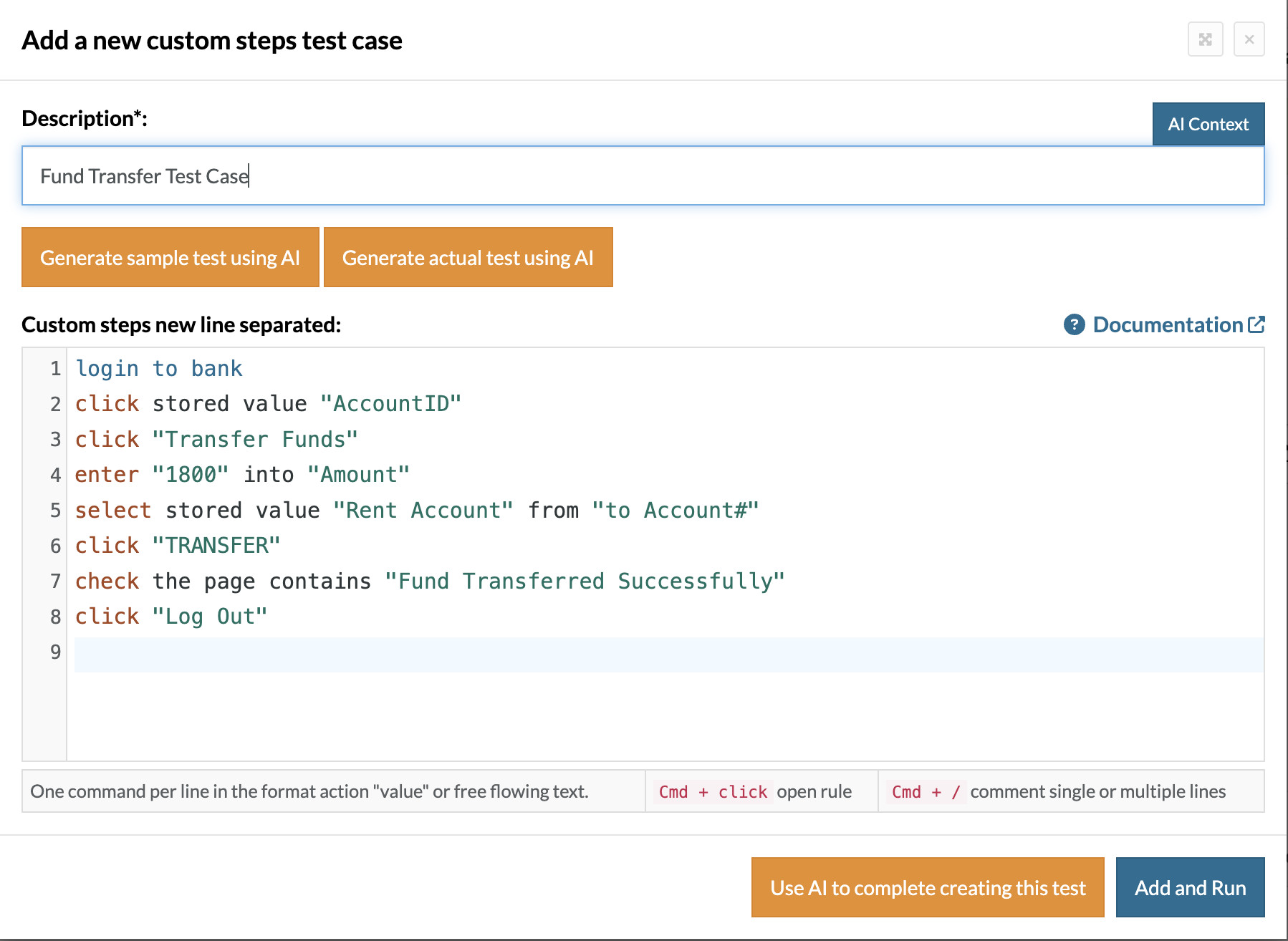

Let’s see how we can create a few test cases using testRigor.

enter stored value "CustomerID" into "Username" enter stored value "customerPassword" into "Password" Click "LOG IN"

The above will be basic steps, used in every test case. So instead of writing these steps every time, we can create reusable rules.

login to bank click stored value "AccountID"

See, the above login steps changed to one short text, which is the re-usable function. Now, again, if you see, we are not calling the actual AccountID value anywhere, we are able to save it as a stored value and use it anywhere in the testcase, thereby giving maximum security to the customer.

login to bank click stored value "AccountID" click "Transfer Funds" enter "1800" into "Amount" select stored value "Rent Account" from "to Account#" click "TRANSFER" check the page contains "Fund Transferred Successfully" click "Log Out"

You can go through other features of testRigor here.

Conclusion

Core banking testing is critical because even a single defect can impact financial accuracy, regulatory compliance, and customer trust at scale. Unlike typical applications, it demands absolute precision in ledger balancing, transaction processing, security, and auditability. Effective testing must cover end-to-end workflows, backend validations, batch processes, and integrations across the banking ecosystem. Modern, resilient automation approaches are essential to handle the complexity, statefulness, and zero-tolerance nature of core banking systems.

| Achieve More Than 90% Test Automation | |

| Step by Step Walkthroughs and Help | |

| 14 Day Free Trial, Cancel Anytime |